What the new rules mean for credit unions and equity securities

Introduction

Utilizing equity securities, like stocks, mutual funds, and exchange-traded funds, has historically been a reasonable way to invest credit union assets. But now, due to updated accounting guidelines, these types of investments may not be as appropriate as they once were.

The financial accounting standards board (fasb) has issued a new guidance that impacts all entities holding financial assets, including credit unions, by changing the standards of an equity security. The guidance forces credit unions to report any losses on stocks, mutual funds, and etfs on their current net income statements, even if those investments are designed to be held for the long-term to meet future obligations like funding executive retirement plans. The guidance came into effect december 15, 2018, and the volatility of equity securities can cause a number of issues for credit unions if they don’t transition their portfolios to more stable and predictable assets soon.

Let’s take a look at what is happening under the fasb’s new guidance, why this change came to pass, and what credit unions can do to ensure that they make the right choices when it comes to equity securities.

https://acumeninsurancesolutions.com/wp-content/uploads/2022/08/Acumen-Credit-Union-Alert-scaled.jpg17072560Shay Larbyhttps://acumeninsurancesolutions.com/wp-content/uploads/2022/07/Acumen_No-Trademark_Brand-Identity_RGB_Signature_Vertical_Full-Color-1030x622.pngShay Larby2021-01-22 14:18:002022-08-04 14:29:11Credit Union Alert FASB Update Now in Effect

Bank Owned Life Insurance (BOLI) is an institutional financial product used by most U.S. banks the first policy was issued in 1983.

BOLI is used to provide benefits to key employees, retain top bank directors and executives, and protect against the loss of a critical employee, in addition to enhancing non-interest income.

The bank is the policy owner, premium payor, and beneficiary the insureds are consenting key executives.

Policies are placed with top-quality insurance carriers and funded on a single premium basis, with cash values growing income tax deferred and death benefits paid income tax-free. 1

Policies with similar characteristics can be used for organizations, families, and individuals to provide protection and enhance current balance sheets.

Who Owns Boli?

Did you know that many commercial banks have more invested in life insurance policies than they do in bank premises, fixed assets and all other real estate assets combined?

As of the third quarter of 2019, nearly 3,800 banks owned $190 billion in BOLI policies. For example, Bank of America owns $22 billion, JP Morgan Chase owns $11 billion, and Wells Fargo owns $18 billion in BOLI assets2.

BOLI is highly regulated by various federal and state banking authorities Regulations allow banks to hold up to 25% of their most vital regulatory capital known as Tier 1 in BOLI policies .3

What is the Purpose of BOLI?

Even though BOLI can be a very attractive place for banks to earn higher current yields on their safest capital, these policies are not purchased for the sole purpose of enhancing non-interest income.

Rather, BOLI is used as a tax-favored asset to increase bank earnings and offset rapidly rising costs of employee benefits, such as sky-rocketing medical, disability, and workers’ comp insurance premiums.

BOLI is also used to protect (indemnify) the bank from the unexpected loss of skilled and valuable executives, often referred to as “key person” life insurance.

Banks also utilize BOLI as a vehicle to finance the cost of providing a deferred compensation plan for key officers.

Download the guide to Bank Owned Life Insurance here:

BOLI is institutionally-priced, permanent life insurance, funded with a single, lump-sum premium.

The premium equals the cash surrender immediately. BOLI products have no-loads, nosurrender charges, and all the income.

How Does BOLI Enhance a Bank’s Balance Sheet?

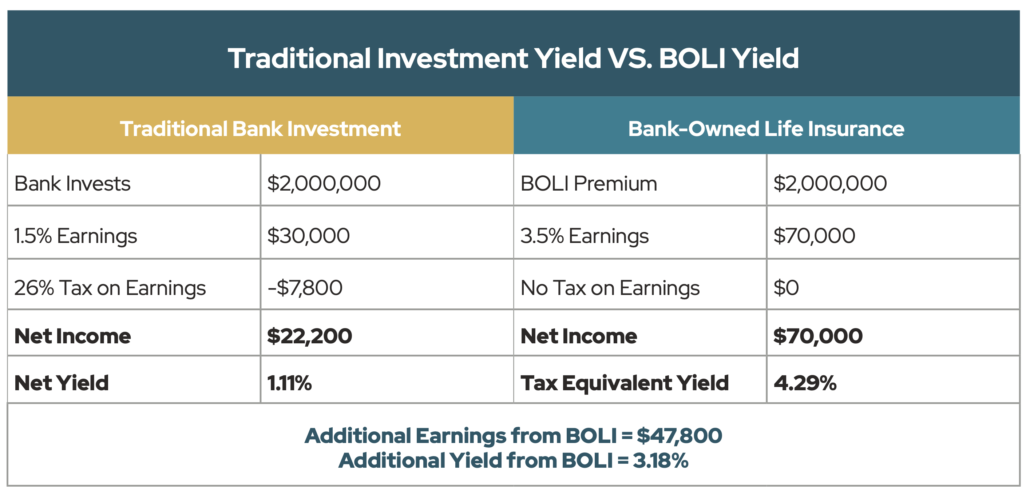

One of the biggest ancillary benefits is that BOLI policies produce far superior returns than traditional bank investments, such as municipal bonds, 5- and 10-year U.S. Treasurys, and mortgage-backed securities (refer to Chart A).

BOLI generates non-taxable profit and loss earnings equal to the growth in cash surrender value, and any death benefits are paid out are completely tax-free.

In fact, the tax advantages enjoyed by using BOLI are usually absent in other nonqualified retirement packages and benefit plans, which is what makes BOLI such a valuable component of a general deferred compensation program.

To emphasize earnings, BOLI policies are structured to maximize the cash value growth and minimize the expense of the death benefit portion of policy.

BOLI is issued by highly-rated insurance companies, which means that the chance for default, bankruptcy, or other negative situations is remote.

In fact, banks and their regulators are comfortable using life insurance companies to protect their safest capital because they do not use excessive leverage.

For example, if a bank has $1 on deposit, it can lend out up to $10 to borrowers. This leverage can lead to instability and, in excess, bank failure or a “run” on the bank where it cannot meet depositor demand.

However, if a life insurance company has the same $1 on deposit, it may loan out no more than $0.92, and usually only a fraction of that amount, which makes them stable institutions in down economies and a good fit for a portion of banks’ safest capital.

Who is BOLI Policy Owner, Insured, and Beneficiary?

The bank is the owner and beneficiary of the policies. When the insured employee passes away this tax-free death benefit can be used to fill the vacuum left by the death of the key executive, as well as fund other business needs.

Banks typically keep the life insurance policies on retired or separated executives because the rate of return can be even higher when the policies are held until death.

A portion of the death benefit may be shared with insured officers via a supplemental life insurance plan which can serve as a valuable “Golden Handcuff.”

Depending on the insurance companies and amount of premium, if 10 or more executives participate, then in most cases no medical tests are required.

Can Individuals Benefit From BOLI?

Life insurance companies only issue institutionally priced BOLI policies to commercial banks.

However, some carriers allow selected agents to design retail policies with loads and fee structures that are like BOLI. These policies are used to protect families against the loss of breadwinners and to protect businesses, including nonprofits, against the loss of owners and key employees.

Just like BOLI, these policies also generate higher current yields on cash value compared to those offered by other safe, liquid assets, such as CDs, U.S. Treasurys, and bonds (refer to Chart B).

https://acumeninsurancesolutions.com/wp-content/uploads/2022/08/What-is-BOLI.jpg14142121Amanda Rogershttps://acumeninsurancesolutions.com/wp-content/uploads/2022/07/Acumen_No-Trademark_Brand-Identity_RGB_Signature_Vertical_Full-Color-1030x622.pngAmanda Rogers2021-01-04 09:17:002022-08-04 09:57:28What is Bank-Owned Life Insurance (BOLI) and How Can You Benefit?

Working from home meant we could vary snack and coffee breaks, change our desks or view, goof off, drink on the job, even spend the day in pajamas, and often meet to gossip or share ideas.

On the other hand, we bossed ourselves around, set impossible goals, and demanded longer hours than office jobs usually entail. It was the ultimate “flextime,” in that it depended on how flexible we felt each day, given deadlines, distractions, and workaholic crescendos.

But on Aristotle’s view, the lives of individual human beings are invariably linked together in a social context. In the Peri PoliV he speculated about the origins of the state, described and assessed the relative merits of various types of government, and listed the obligations of the individual citizen.

Successful people ask better questions.

Aristotle made several efforts to explain how moral conduct contributes to the good life for human agents, including the Eqikh EudaimonhV and the Magna Moralia, but the most complete surviving statement of his views on morality occurs in the Eqikh Nikomacoi.

Working from home meant we could vary snack and coffee breaks, change our desks or view, goof off, drink on the job, even spend the day in pajamas, and often meet to gossip or share ideas. On the other hand, we bossed ourselves around, set impossible goals, and demanded longer hours than office jobs usually entail. It was the ultimate “flextime,” in that it depended on how flexible we felt each day, given deadlines, distractions, and workaholic crescendos.

Aristotle made several efforts to explain how moral conduct contributes to the good life for human agents, including the Eqikh EudaimonhV and the Magna Moralia, but the most complete surviving statement of his views on morality occurs in the Eqikh Nikomacoi.

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.