How Can Your Nonprofit Keep Pace with Rising Costs?

Charitable organizations are seeing their donations decrease in value due to inflation. In order to keep pace with rising costs, it is important for nonprofit organizations to diversify their assets. This will help protect them from the negative effects of inflation and ensure that they can continue to serve their communities effectively.

In this blog, we will explore how inflation has impacted nonprofits and ways to combat that.

Inflation Is a Problem

Inflation has become a problem for nonprofits because now:

- They have to spend more money to maintain the same level of services

- Their funding doesn’t keep pace with inflation

- It’s harder to attract and retain donors

- Their overhead costs go up while their funding remains stagnant

Therefore,

- It can lead to cuts in programs or services

- It can force nonprofits to make difficult choices about how to allocate their resources

- It can put pressure on staff and volunteers

- It can make it difficult to plan for the future

Inflation-Proof Your Portfolio

When choosing investments, nonprofit organizations should consider both stocks and bonds. They should also look into assets like life insurance, which can help protect against inflation. By diversifying their portfolios, nonprofit organizations can keep pace with rising costs.

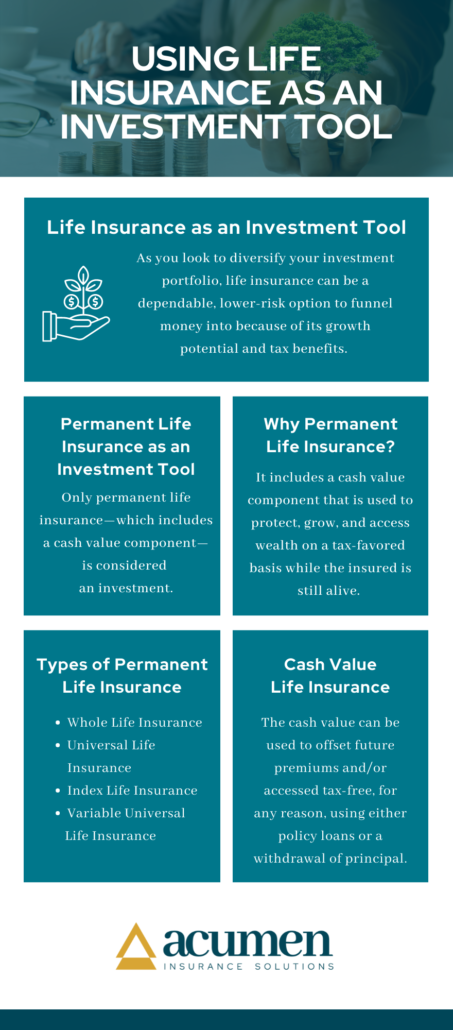

How Insurance Can Help Inflation-Proof Your Portfolio

While stocks and bonds are important investments for nonprofit organizations, insurance can also play a role in protecting against inflation. Insurance is a safe and liquid option that can help to inflation-proof your portfolio.

When choosing an insurance policy, nonprofit organizations should consider both the death benefit and the cash value of the policy. The death benefit will provide protection in the event of the death of a key member of the organization, while the cash value grows at a competitive rate and can be used to cover expenses in times of need.

Nonprofit organizations should consider purchasing an insurance policy with a high death benefit and a cash value that grows over time with a positive correlation to rising interest rates.

Don’t Forget About Other Investments

While stocks and bonds are important investments for nonprofit organizations, it is also important to diversify your portfolio with other assets. These assets could include real estate, art, or even cryptocurrency.

Other Simple Steps to Offset Inflation

1. Understand what inflation is and how it can impact your nonprofit.

2. Look for ways to increase revenue without raising prices.

3. Consider alternative sources of funding.

4. Invest in assets that will appreciate over time.

5. Review your budget regularly and make adjustments as needed.

6. Be prepared to make changes in your operations if necessary.

7. Educate your staff and volunteers about inflation and how it can affect your nonprofit.

8. Keep a close eye on your expenses and look for ways to cut costs.

9. Advocate for policies that help nonprofits offset the impact of inflation.

10. Remain adaptable in the face of change.

Final Thoughts

Nonprofit organizations face many challenges, but by diversifying their portfolios they can keep pace with rising costs and continue to serve their communities effectively. By considering both stocks, bonds, and assets like insurance, nonprofit organizations can protect themselves from inflation and ensure the longevity of their charity.

Have any questions? Contact us to learn more about how you can help protect your nonprofit from rising costs.