What is Bank-Owned Life Insurance (BOLI) and How Can You Benefit?

Bank Owned Life Insurance (BOLI) is an institutional financial product used by most U.S. banks the first policy was issued in 1983.

BOLI is used to provide benefits to key employees, retain top bank directors and executives, and protect against the loss of a critical employee, in addition to enhancing non-interest income.

The bank is the policy owner, premium payor, and beneficiary the insureds are consenting key executives.

Policies are placed with top-quality insurance carriers and funded on a single premium basis, with cash values growing income tax deferred and death benefits paid income tax-free. 1

Policies with similar characteristics can be used for organizations, families, and individuals to provide protection and enhance current balance sheets.

Who Owns Boli?

Did you know that many commercial banks have more invested in life insurance policies than they do in bank premises, fixed assets and all other real estate assets combined?

As of the third quarter of 2019, nearly 3,800 banks owned $190 billion in BOLI policies. For example, Bank of America owns $22 billion, JP Morgan Chase owns $11 billion, and Wells Fargo owns $18 billion in BOLI assets2.

BOLI is highly regulated by various federal and state banking authorities Regulations allow banks to hold up to 25% of their most vital regulatory capital known as Tier 1 in BOLI policies .3

What is the Purpose of BOLI?

Even though BOLI can be a very attractive place for banks to earn higher current yields on their safest capital, these policies are not purchased for the sole purpose of enhancing non-interest income.

Rather, BOLI is used as a tax-favored asset to increase bank earnings and offset rapidly rising costs of employee benefits, such as sky-rocketing medical, disability, and workers’ comp insurance premiums.

BOLI is also used to protect (indemnify) the bank from the unexpected loss of skilled and valuable executives, often referred to as “key person” life insurance.

Banks also utilize BOLI as a vehicle to finance the cost of providing a deferred compensation plan for key officers.

Download the guide to Bank Owned Life Insurance here:

How is BOLI Funded?

BOLI is institutionally-priced, permanent life insurance, funded with a single, lump-sum premium.

The premium equals the cash surrender immediately. BOLI products have no-loads, nosurrender charges, and all the income.

How Does BOLI Enhance a Bank’s Balance Sheet?

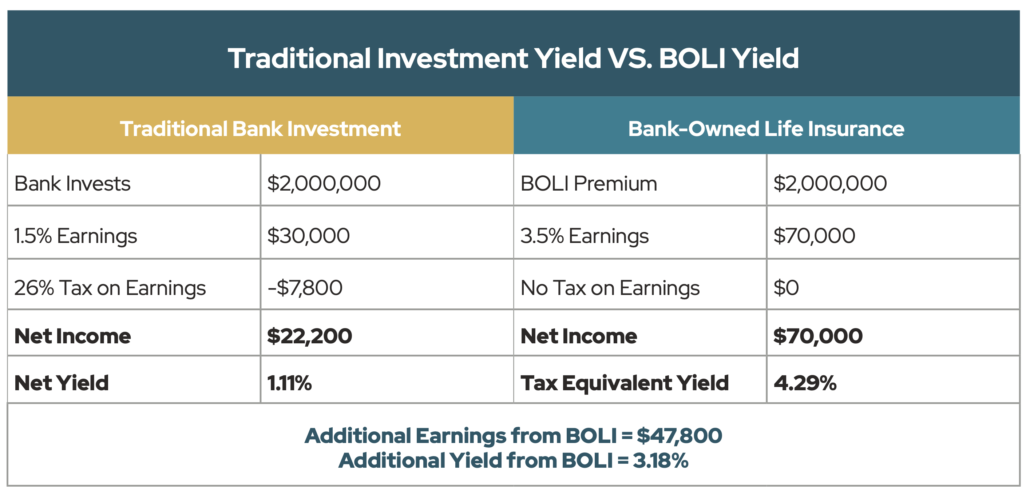

One of the biggest ancillary benefits is that BOLI policies produce far superior returns than traditional bank investments, such as municipal bonds, 5- and 10-year U.S. Treasurys, and mortgage-backed securities (refer to Chart A).

BOLI generates non-taxable profit and loss earnings equal to the growth in cash surrender value, and any death benefits are paid out are completely tax-free.

In fact, the tax advantages enjoyed by using BOLI are usually absent in other nonqualified retirement packages and benefit plans, which is what makes BOLI such a valuable component of a general deferred compensation program.

To emphasize earnings, BOLI policies are structured to maximize the cash value growth and minimize the expense of the death benefit portion of policy.

BOLI is issued by highly-rated insurance companies, which means that the chance for default, bankruptcy, or other negative situations is remote.

In fact, banks and their regulators are comfortable using life insurance companies to protect their safest capital because they do not use excessive leverage.

For example, if a bank has $1 on deposit, it can lend out up to $10 to borrowers. This leverage can lead to instability and, in excess, bank failure or a “run” on the bank where it cannot meet depositor demand.

However, if a life insurance company has the same $1 on deposit, it may loan out no more than $0.92, and usually only a fraction of that amount, which makes them stable institutions in down economies and a good fit for a portion of banks’ safest capital.

Who is BOLI Policy Owner, Insured, and Beneficiary?

The bank is the owner and beneficiary of the policies. When the insured employee passes away this tax-free death benefit can be used to fill the vacuum left by the death of the key executive, as well as fund other business needs.

Banks typically keep the life insurance policies on retired or separated executives because the rate of return can be even higher when the policies are held until death.

A portion of the death benefit may be shared with insured officers via a supplemental life insurance plan which can serve as a valuable “Golden Handcuff.”

Depending on the insurance companies and amount of premium, if 10 or more executives participate, then in most cases no medical tests are required.

Can Individuals Benefit From BOLI?

Life insurance companies only issue institutionally priced BOLI policies to commercial banks.

However, some carriers allow selected agents to design retail policies with loads and fee structures that are like BOLI. These policies are used to protect families against the loss of breadwinners and to protect businesses, including nonprofits, against the loss of owners and key employees.

Just like BOLI, these policies also generate higher current yields on cash value compared to those offered by other safe, liquid assets, such as CDs, U.S. Treasurys, and bonds (refer to Chart B).