Why Do Credit Unions Use Corporate-Owned Life Insurance (COLI)?

Credit unions use the cash value of Corporate-Owned Life Insurance (COLI) as a tool to help them generate higher yields to offset the rising costs associated with employee benefits programs, such as health insurance and retirement.

The death benefit from a life insurance policy can be used to help the organization shore-up underfunded benefit programs, pay off debts, fund future expenses, or even shared with the insured employee’s family to provide financial security.

Scott B. Hinkle, Principal at Acumen Insurance Solutions and the leader of the firm’s Credit Union practice, explains more in the video.

What is Corporate-Owned Life Insurance?

Corporate-Owned Life Insurance (COLI) is a type of life insurance policy that is owned by a company and pays benefits to the company upon the death of the insured employee. The premiums for COLI policies are paid by the company, making them an attractive way for businesses to provide death benefits to the organization and, potentially, its key employees.

When properly structured, the death benefit from a COLI policy can be received tax-free by the company and policy beneficiaries, making them an effective tool for tax and estate planning.

See another video from Scott and learn more about COLI in our Mark-to-Market and COLI blog.

Reasons Credit Unions use COLI

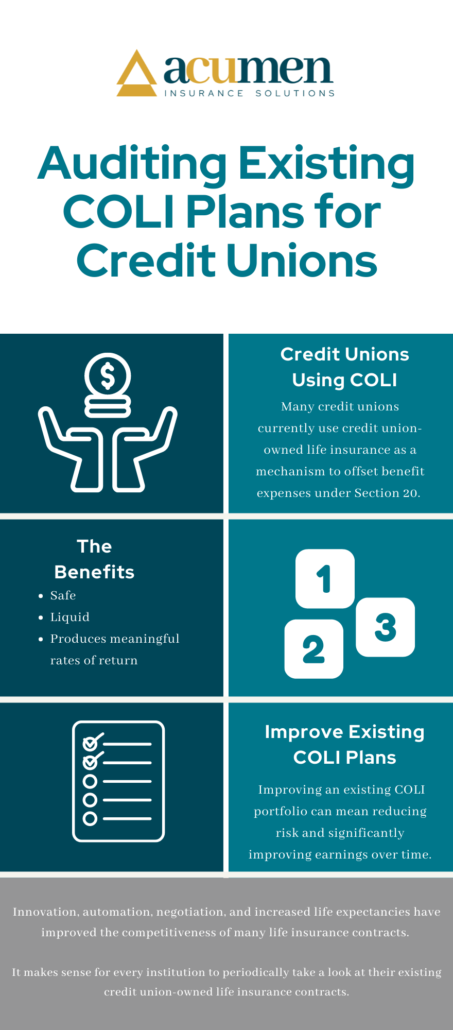

There are a few reasons why credit unions might choose to use COLI. First, it can be a way to generate additional income for the credit union. This income can then be used to help offset operating costs or to fund other activities.

Additionally, COLI can also help to diversify the credit union’s investment portfolio. By investing in COLI, the credit union can reduce its overall risk.

COLI can also provide death benefits to the insured executive’s families as a benefit of employment with the credit union, which can help the organization attract and retain its key people.

Credit unions may also use COLI cash value earnings to fund executive retirement programs. These programs provide key executives with additional financial incentives to stay with the credit union and continue to perform at a high level.

Takeaways from Scott

The NCUA (National Credit Union Administration) code allows credit unions to invest in financial instruments that they otherwise would not be able to invest in, with the goal being able to offset the rapidly-rising costs of employee benefit expenses.

The NCUA realizes that the way most credit unions invest with the bulk of their assets is very conservative, and therefore has a historically lower rate of return. For many credit unions, they invest most of their assets in 10 years or less debt securities or bonds, which have a certain yield profile.

However, under this Section 20 of the Call Report, the NCUA allows credit unions to invest in what are called otherwise impermissible investments, which have the potential to earn more than traditional investments while still maintaining a very high level of safety and liquidity.

Life insurance contracts are one type of otherwise impermissible investment, and they offer the credit union a higher rate of return, a death benefit, and safety. The goal is for the credit union to use these alternative investments to keep up with the rising cost of benefit expenses.

A Final Word

Credit unions and nonprofits have to provide good benefits, but the ways they are allowed to make money from investments is very limited. Section 20 of a credit union’s Call Report lists the “otherwise impermissible” investments like COLI, where the yields can be higher. They can do this to offset the rising costs of executive compensations (ie: benefits like health insurance and 401(k) matching), which would be too expensive otherwise.

Read on to learn about how COLI can help fund executive comp packages.

COLI can be a very valuable tool for credit unions. To find out more about how COLI can benefit your credit union, reach out to us today!